Now more than ever, recent court precedence has created the need to partner with a firm that understands your industry to maximize Research & Development tax credits. This article explains the result of Little Sandy Coal vs. Commissioner and why it’s important to every organization.

How Did We Get Here?As discussed in our previous post, Little Sandy Coal received an unfavorable outcome to its suit for redetermination after an IRS notice of deficiency related to its Research & Development (R&D) tax credits claimed under Section 41. The US Tax Court’s 2021 memorandum opinion upheld the tax deficiency as well as an accuracy-related penalty. The court’s holding largely turned on the taxpayer’s failure to demonstrate that “substantially all” - a statutory threshold of 80% or more - of the taxpayer’s research activities relating to each of the projects at issue constituted elements of a process of experimentation.

The taxpayer appealed the tax court’s decision, arguing that the “substantially all” test was misapplied to the projects at issue. Specifically, because the vessels were first-in-class and most of each unit was new, the projects reached the 80% threshold. To bolster this argument, the taxpayer relied heavily on the opinions in Trinity Industries, Inc. v. United States. 691 F. Supp. 2d 688 (N.D. Tex. 2010), aff’d, 757 F.3d 400 (5th Cir. 2014).

Additionally, the taxpayer argued that because the tax court agreed that there were qualified activities, then the court should at a minimum estimate the qualified portion of the expense, applying long-standing principles affirmed by the Fifth Circuit in United States v. McFerrin. 570 F.3d 672, 679 (5th Cir. 2009) (citing Cohan v. Comm’r, 39 F.2d 540, 544 (2d Cir. 1930)).

Ultimately, the taxpayer’s arguments were unpersuasive. The appeals court found that the taxpayer had not provided substantiation for its assertion that 80% or more of the activities on each of the claimed projects constituted a process of experimentation and because the taxpayer failed to satisfy that threshold, there were no eligible qualifying expenses under Section 41.

Learn More: Little Sandy Coal Company v. Commissioner |

The Court's Reasoning

To evaluate whether the taxpayer met its burden of proof, the court reviewed the tax court’s factual analysis for clear error and its interpretation of the law de novo. The court acknowledged that only the requirement at issue for the claimed project was whether “substantially all of such activities were research activities that constitute elements of a process of experimentation.” The remainder of the elements for the four-part test were not at issue.

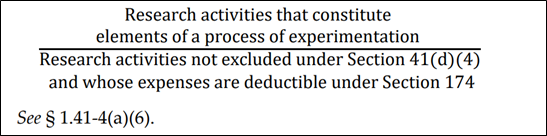

As an initial matter, the Seventh Circuit confirmed the appropriate “substantially all” calculation for the evaluation of new or improved business components, displayed below.

However, the court diverged from the tax court’s treatment of wage expenses for direct support and supervision within the fraction. The court clarified that all expenses properly includable for qualified activities and deductible under Section 174, including direct support and direct supervision, should be incorporated in both the numerator and denominator. This interpretation provides a more generous calculation compared to the analysis performed at the tax court level.

Further, the court explained that the evaluation of qualified activities that constitute a process of experimentation as compared to the total research activities is the only appropriate test for determining whether a project meets the “substantially all” (80%) threshold. Citing Section 1.41-4(a)(6), the court affirmed that the “substantially all” test must be applied to activities “on a cost or other consistently applied reasonable basis,” not the “physical elements of the business components being developed or improved” and that the “novelty of the business component cannot be the basis for measuring the proportion of research activities that constituted elements of a process of experimentation.” Specifically, the court rejected the Trinity courts’ analysis in which two out of six vessels reviewed were found to meet the “substantially all” test without reference to any activities or expenses during the design and development of the ships. While there are distinctions to be drawn in the facts surrounding Trinity’s inability to provide additional information, going forward, taxpayers will need to carefully distinguish the activities associated with the required process of experimentation.

Additionally, the court addressed the production expenses claimed for the first-in-class vessels. The court clarified the appropriate analysis for the inclusion of “pilot model” expenses, including potentially qualified supplies and production wages to manufacture the vessels. The court stated the definition of pilot models under Section 174 as “any representation or model of a product that is produced to evaluate and resolve uncertainty concerning the product during the development or improvement of the product.” § 1.174-2(a)(4). Further, the court explained that the “model must be used to evaluate one or more alternatives using the scientific method” to constitute an element of the process of experimentation. With this, the court confirmed that for properly qualified pilot models, production expenses are accurately included in the denominator of the “substantially all” analysis, and if the models are built to resolve uncertainty regarding the product’s development, they may also be included in the numerator.

Taxpayer's Failure of Proof

With its legal framework established, the court turned to apply its analysis to the facts presented. Just as the lower court did, the Seventh Circuit recognized that activities on certain aspects of the vessels likely constituted elements of a process of experimentation. Similarly, the court opined that the vessels could have been produced to resolve uncertainty during the development of the new products. However, the court found that the taxpayer lacked the documentation regarding the portion of activities and expenses on each vessel that constituted a process of experimentation. Because the taxpayer relied on the novelty of the units for qualification, documentation was not provided as to the activities on components of the vessels or time apportioned to the more challenging aspects of the design. Further, the taxpayer was unable to tie the non-production wages to the vessels claimed and likewise could not distinguish between generally qualified activities performed by those employees and activities associated with the process of experimentation.

The court did not reach the issue of whether the first-in-class vessels produced by the taxpayer were pilot models because the evidence presented failed to convince the court that the activities and associated wage expenses for each vessel constituted elements of a process of experimentation.

Takeaways

It is important to note that the disallowance of the credits was based on the facts of this case and the documentation available to the appellate and trial courts. The court said it best:

The lesson for taxpayers seeking to avail themselves of the research tax credit is to adequately document that “substantially all” of such activities were research activities that constitute elements of a process of experimentation. Generalized descriptions of uncertainty, assertions of novelty, and arbitrary estimates of time-performing experimentation are not enough.

As the courts continue to emphasize the importance of substantiation, it is critical to partner with a firm that understands the documentation available by industry and what is necessary to best support a taxpayer’s R&D tax credit claim. Contact CTI today and let our team of R&D experts work to maximize your credit and help you gather, produce, and maintain a substantiation package tailored to satisfy the latest case law and regulatory changes.